Smart Home Buying: Maximize Your Savings with a Seller Credit

When purchasing a home, negotiating with the seller can significantly impact your monthly budget. A common strategy is to ask for a price reduction, but did you know that requesting a seller credit to buy down your interest rate could save you much more? Let’s break down this pro tip and explore how it can work for you.

The Traditional Approach: Price Reduction

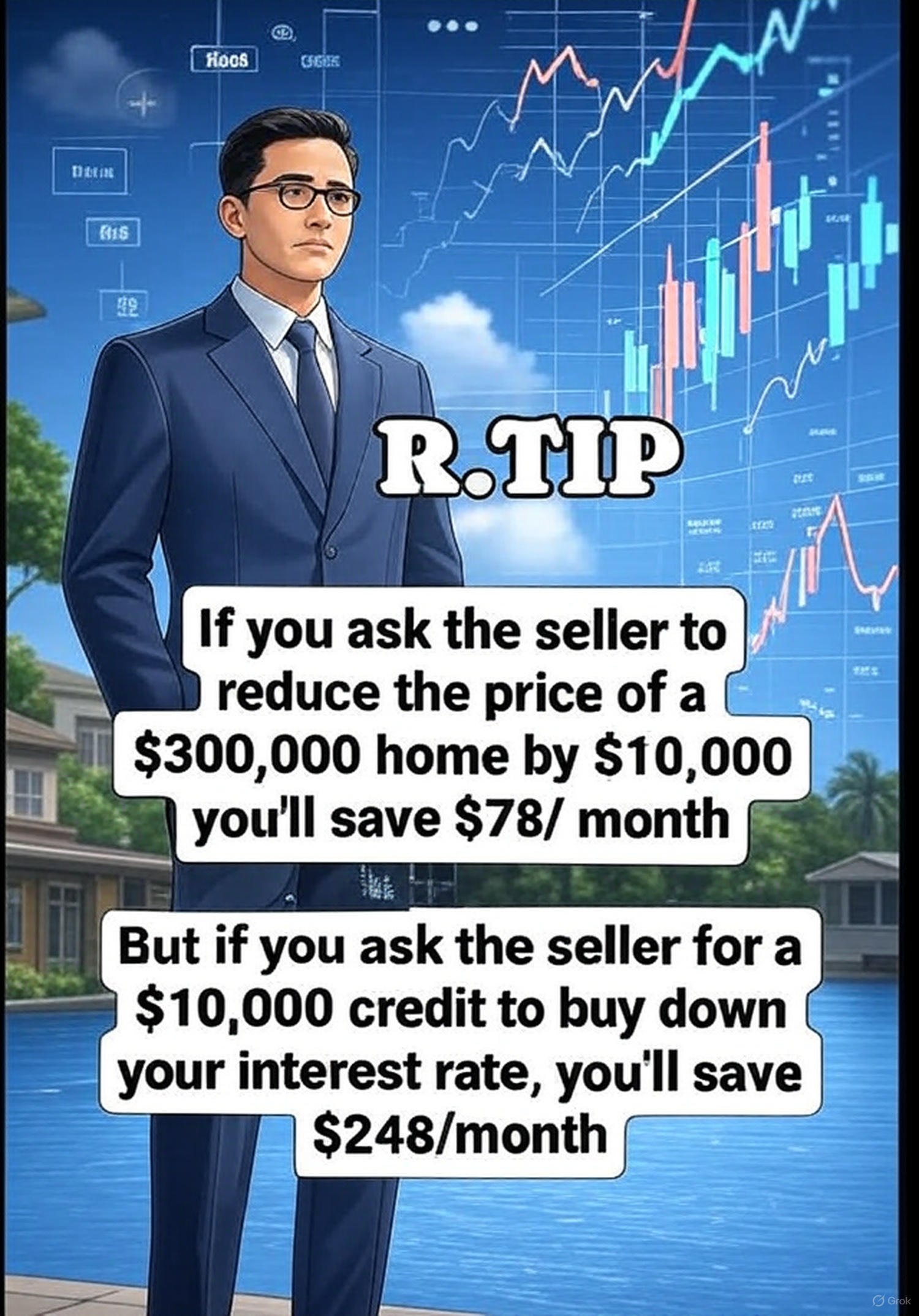

If you ask the seller to reduce the price of a $300,000 home by $10,000, you might think you’ve scored a great deal. On the surface, this seems like a straightforward saving. However, the monthly impact is relatively modest. With a price reduction of $10,000, your monthly mortgage payment could decrease by approximately $78, assuming a standard 30-year fixed-rate mortgage at current interest rates. While this is a welcome saving, it’s not the most impactful option available.

The Smarter Strategy: Seller Credit for Interest Rate Buy-Down

Now, consider an alternative: asking the seller for a $10,000 credit to buy down your interest rate. This approach can have a much larger effect on your monthly payments. By using the credit to reduce your interest rate—potentially lowering it by 0.5% to 1% depending on the lender and loan terms—you could save around $248 per month on that same $300,000 home. This is over three times the savings of a direct price reduction!

Why the Difference?

The key lies in how interest rates compound over the life of a loan. A lower interest rate reduces the total interest paid over time, which translates to a bigger monthly saving compared to a one-time price cut. For example, a $10,000 price reduction lowers the principal, but the interest rate remains unchanged, limiting the monthly benefit. In contrast, a rate buy-down reduces the interest rate across the entire loan term, amplifying your savings month after month.

How to Negotiate This

1 Research Current Rates: Understand the prevailing mortgage rates and how much a $10,000 credit could lower your rate. Consult with your lender for specifics.

2 Make the Offer: Propose the seller credit as part of your offer. Highlight that it benefits both parties— you get lower payments, and the seller can still sell at their desired price.

3 Work with Your Lender: Ensure the credit is applied correctly to buy down the rate, maximizing your savings.

Final Thoughts

When house hunting, think beyond the sticker price. A $10,000 seller credit to buy down your interest rate can offer substantial long-term savings compared to a simple price reduction. On a $300,000 home, this strategy could save you $248 per month versus $78, making a significant difference in your financial planning. As you prepare for your next home purchase, consider discussing this option with your real estate agent and lender to see how it fits your goals.

Happy house hunting, and smart negotiating!

No Comments